Parag Patadiya

Partner - Head of Assurance Services

Background

IFRS 9 introduces new requirements that affect entities across all industry sectors. Although it is true that the most significant effects are faced by entities in the financial sector, it is proven to be a common mistake to assume that there are limited effects elsewhere.

Steps to implementation

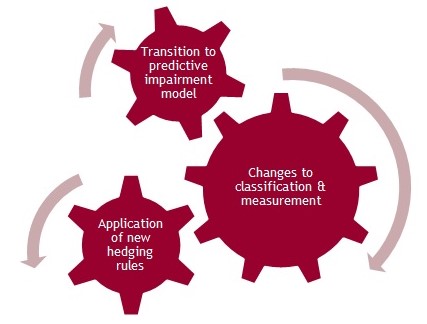

The adoption of IFRS 9 should be considered in three distinct phases:

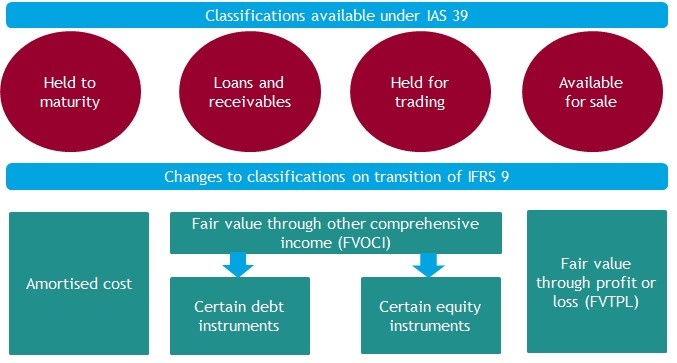

Classification & Measurement

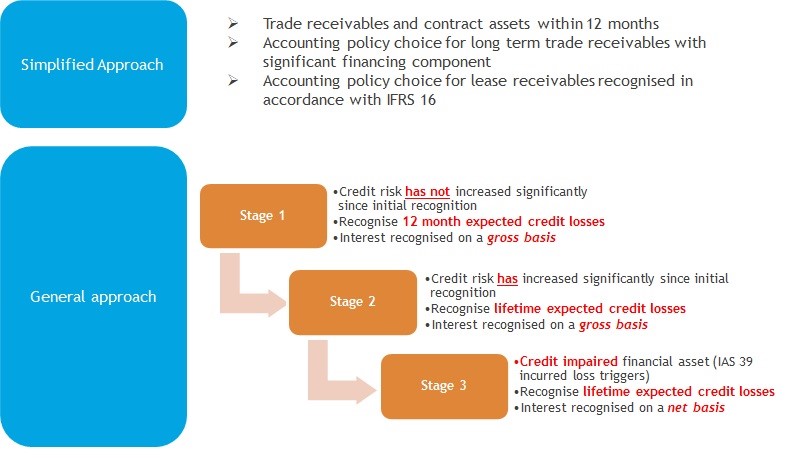

Impairment

Questions which should be asked for adoption include:

Project management, Board sponsorship and communication with those charged with governance:

Detailed effects:

Performing a detailed impact assessment of the adoption of IFRS 9.

Providing assistance with the quantification of adjustments at the date of initial application and reporting date relating to both classification and measurement (C&M) and expected credit losses (ECL).

Providing assistance in complying with the new hedge requirements and performing hedge effectiveness testing.

For more details and guidance on IFRS 9 application, please see IFRS Publications by BDO.